A new Systemiq report shows that scaling clean energy investment in emerging markets and developing economies will depend on using development and catalytic finance differently. By shifting to a more catalytic system, far less public finance could be required to mobilise the private finance needed for the energy transition.

Emerging markets and developing economies (EMDEs) are at the centre of the global energy transition. They are home to 70% of the world’s population and hold most of its renewable energy potential. They will also drive the fastest growth in energy demand.

Yet today, these countries receive just 15% of global clean energy investment.

Meeting demand by 2035 will require a six-fold increase in investment. At the same time, public budgets are under pressure and development finance is constrained. This means, without mobilising private capital at scale, the global energy transition will fall short.

While the magnitude of the investment gap is widely recognised, the discussion to date has focused on aggregate investment need figures with limited guidance for practical action.

Systemiq’s new report, The Private Finance Mobilisation Gap, provides new insights into how much private investment can realistically be mobilised, and what type of development and catalytic finance is needed to unlock it.

A $1.3 trillion opportunity held back by risk

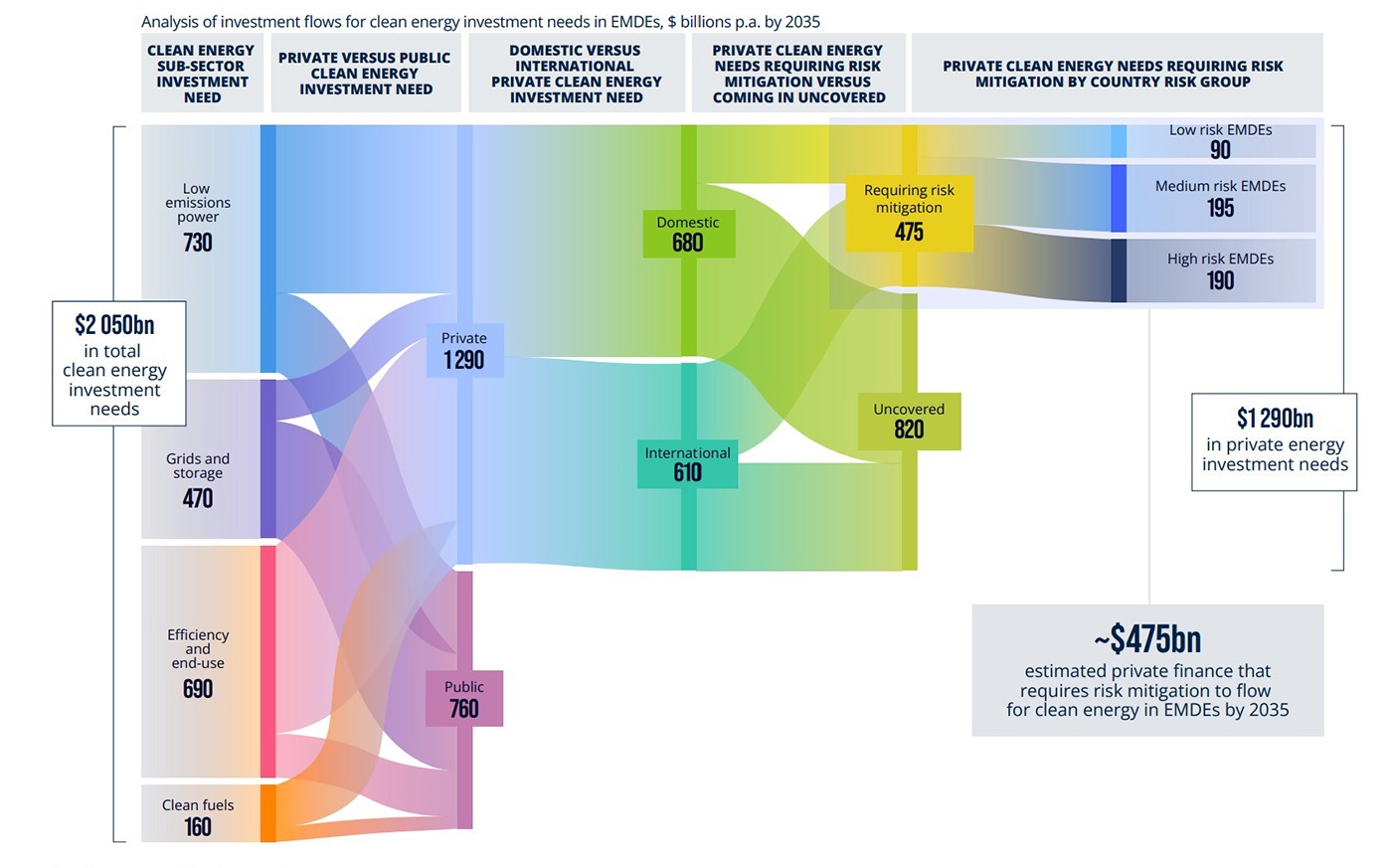

The report shows that the opportunity for private investment is significant. By 2035, almost $1.3 trillion in clean energy each year across EMDEs could be financed by the private sector – almost two-thirds of total investment needs.

However, much of this capital is not flowing today. By 2035, around $475 billion of investment is estimated to sit outside investors’ risk appetite due to barriers such as currency volatility, political uncertainty and early-stage technology risk.

Analysis of investment flows for clean energy investment needs in EMDEs, $ billiond p.a. by 2035

Development and catalytic finance, provided primarily by multilateral development banks (MDBs), development finance institutions (DFIs) and donors, is needed to address these barriers, help build markets and mobilise private investment.

But our report finds that it is not being used effectively.

Historically, $2 of public finance has mobilised just $1 of private investment in EMDE clean energy. Much of this finance is delivered as market-rate debt, which is not designed to crowd in private capital.

If this approach continues, nearly $1 trillion in public and catalytic finance would be needed every year by 2035 to mobilise the $475 billion of private finance estimated to require some form of risk mitigation to flow towards clean energy in EMDEs, which is an unachievable level.

The unlock: shifting to a more catalytic system

Despite growing awareness and ongoing reforms, private capital mobilisation remains below the scale and pace required. The report shows that shifting development and catalytic finance providers’ portfolios to use more catalytic finance like guarantees, catalytic equity and local currency finance could dramatically improve outcomes. These forms of finance are far better at mobilising private finance but are under-utilised today.

Under this more ambitious approach, the amount of development and catalytic finance needed could fall by more than half – from nearly $1 trillion to around $430 billion annually by 2035.

The key is to move away from traditional lending models and towards tools that actively manage, reduce and share risk, help build markets and attract investment at scale. This would make global climate targets more achievable while unlocking significantly more private capital.

Why this matters now for climate finance

With declining aid budgets and public finances under pressure, the need to use scarce public finance more effectively has never been greater. The current system is not delivering the level of private investment needed for the energy transition in EMDEs.

Policymakers, MDBs, DFIs and investors should see that scaling finance is not only about increasing volumes, but about improving how finance is deployed. Done right, this shift could unlock orders of magnitude more private investment where it is needed most while using public finance far more efficiently to do so.

The report highlights the need for urgent reform and transformation across the development finance system. This includes embedding mobilisation into institutional mandates, expanding the use of more risk-bearing instruments, a greater focus on building markets and increasing the capacity of MDBs and DFIs to take on more risk.