A consultation paper by Systemiq in partnership with the Gordon and Betty Moore Foundation · 2026

This consultation paper synthesizes the available evidence into a central hypothesis: that China has begun to apply to food and agriculture some of the same system-level tools it has previously used in sectors such as energy and transport. It considers what that could mean for domestic production, global trade flows and the future of protein supply. The purpose of this paper is to invite discussion on the assumptions, signals and scenarios presented and to use this to collectively shape more sustainable outcomes for all stakeholders involved.

Key Findings

Food security has become a strategic priority for Chinese leadership, central to economic stability and national security.

Early signals suggest Beijing is applying the same industrial playbook that is delivering global leadership in solar and EVs to food and agriculture – aligning policy, capital and technology.

By 2030, Chinese import demand will have peaked and begun to fall, especially for feed and animal protein. Demand for imported soya beans is projected to fall by 25%.

Long term, China’s prioritisation of biomanufacturing and alternative protein technologies is set to transform domestic markets and reshape global food production.

Producers who adapt early – diversifying markets, upgrading productivity, raising deforestation and traceability standards – are best placed to succeed in this changing landscape.

Research Summary

For two decades, China has been the engine of global agricultural demand.

That era is now ending. Recent climate shocks, geopolitical tensions and trade disputes have exposed the vulnerability of China’s food system. In response, China’s leadership has elevated food security and sovereignty to a core pillar of national security – placed alongside energy and finance in the 14th Five-Year Plan and deepened further in the 15th. Early indicators suggest that China is applying the same industrial strategy that catalysed its global leadership in solar and electric vehicles to food production.

The picture emerging is that China may be at Year 0 of a broader food system transformation. New food security legislation, state investment in fermentation infrastructure and the emergence of alternative protein clusters all point in a similar direction. The new Five-Year Plan will significantly accelerate this shift, embedding food security and sovereignty as a strategic priority.

Systemiq’s new consultation paper ‘China’s Food Future’ explores how China’s evolving food strategy could reshape its role in global agricultural markets. The report finds that China is set to shift from the world’s largest food importer to a major exporter, with significant implications for producer countries.

Three phases of change

Looking ahead to the next three decades, our analysis identifies the following plausible futures:

By 2030 – Peak imports, target-led optimization and efficiency gains Import demand will have peaked and begun to fall, driven by target-led optimization. Efficiency gains and productivity optimization could erase 25% of China’s soy demand – almost equivalent to all US soybean exports to China in 2024 and comes alongside reductions in beef, poultry, dairy and egg imports.

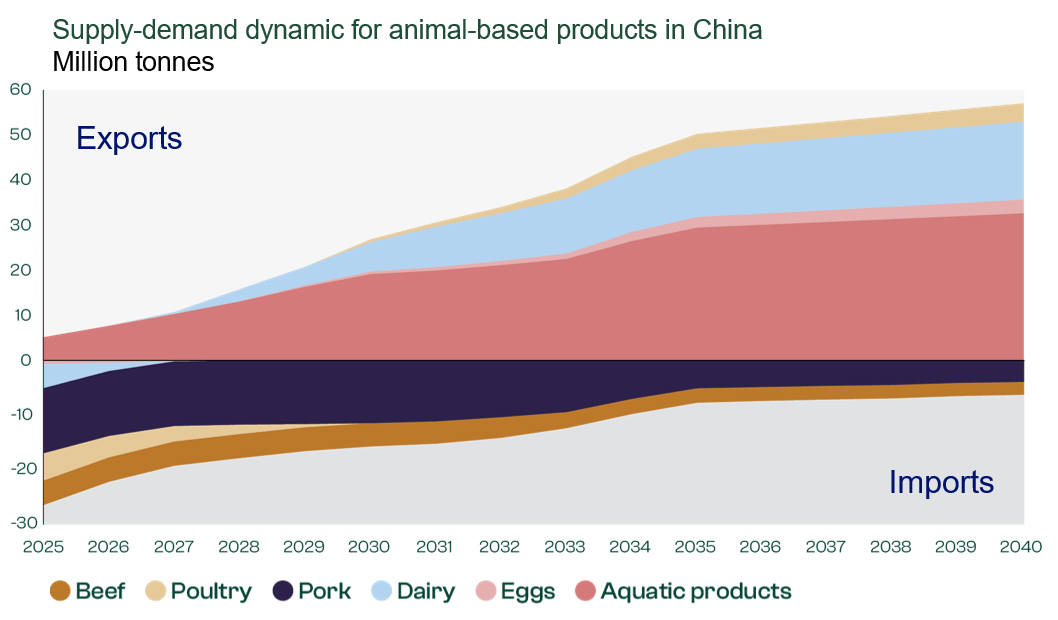

By 2040 – China emerges as a net food exporter Alternative proteins capture a meaningful share of the market as fermentation-derived and plant-based proteins reach price parity with their animal-based equivalents. China becomes a net exporter of poultry, dairy, eggs and aquatic products, introducing Chinese food exports as a competitive force in global markets for the first time.

By 2050 – A new bio-based industry leader A third wave of innovation makes cultivated meats commercially viable. Alternative proteins are projected to meet 35-55% of domestic animal protein demand. China’s role in global protein markets has fundamentally shifted and their leadership in food innovation has once again made it the world’s leading supplier of a defining 21st century technology.

Implications for global trade and producer countries

The consequences of this transition would be felt across the global food system. China is the primary destination for 89% of Argentina’s soya exports, as well as 71% of Brazil’s, and 53% of the United States’. At the same time, it absorbs a significant amount of Argentina, Brazil, and New Zealand’s beef exports. For these economies, a sustained contraction in Chinese demand not only reduces volumes but risks simultaneous falls in price and export revenue.

Producer countries can strengthen their resilience by improving productivity on existing farmland, advancing deforestation and conversion-free (DCF) and traceability standards, diversifying markets, and reducing exposure to demand shifts while avoiding investments that may not generate the expected returns. These approaches will help them maintain access to higher-value markets with stricter traceability requirements.

The alternative protein industry can also expect reduced costs of fermentation infrastructure and increased competition. Accelerated innovation will help companies remain resilient and competitive.