Norway is globally recognised for its ambition to create a thriving low-emissions circular plastic economy that allows sectors to develop without negative – or, ideally, with positive – impacts on the environment, the economy, and society at large. This is both critically important and extremely challenging as the starting point is a highly linear plastic system that emits large amounts of greenhouse gases (GHGs) during both fossil based plastic manufacturing processes and end-of-life incineration. Without transformative changes, the situation is set to get worse in the next years as the plastic accumulating in the system reaches the end of its lifetime and starts to churn out as waste in higher volumes.

Executive

Summary

Fortunately, there is growing awareness of the extent of the problem, and momentum to act is building in terms of both government policies and industry actions around the world. But initiatives are still primarily at the pilot stage and the major shifts needed are yet to occur.

Norway is leading the way in several areas of innovation and is well-positioned to play a pioneering role in the transition to a low-emissions circular plastic system.

The country must now make strategic decisions that will determine the speed and direction of this transition for decades to come.

Coupled with Part 1 of the Achieving Circularity study, this report offers a pioneering vision for how to transform the Norwegian plastic system by 2040. It presents tailored circularity strategies for durable plastics across five very distinct sectors: Construction, Textiles, Electronics & Electrical, Automotive, and Fisheries & Aquaculture.

To define the most effective upstream and downstream strategies for each sector, as well as the policies and partnerships needed to achieve them, we must first analyse the different uses of plastic across sectors in detail, including applications, functionalities, usage forecasts, impacts, and substitutes. Our analysis aims to deepen understanding of the economic, environmental and social implications of the critical choices facing the plastic industry.

Our central goal is to help decision makers and industry leaders in Norway to identify the best pathway to achieve the low-emissions circular plastic system the country needs by modelling three scenarios. The first is a Baseline or Current Commitments Scenario, presenting what the plastic system will look like in 2040 if nothing changes.

Next is the System Change Scenario, which shows the maximum level of circularity that can be achieved by 2040 by scaling up levers such as better waste collection, product design, new delivery models, and recycling. This offers a high level of circularity, but only addresses half the GHG emissions in the plastic system, leading to the third option, the Net-Zero Scenario. This presents a viable pathway for Norway’s plastic system to achieve ~77% circularity and reduce GHG emissions by ~90% by 2040, thus aligning itself with the Paris Agreement.

The fact that Norway imports most of its plastic and plastic products, and exports over a third of its plastic waste, has implications for how to assess both the impacts of its current plastic system and analyse prospective strategies, and is therefore considered across the report’s key findings.

Issues to be addressed include plastic production emissions not being included in Norway’s Nationally Determined Contributions to the Paris Agreement, the majority of jobs being outside Norway, and the need for collaboration with other Nordic countries and the EU to define future plastic solutions. Cooperation will be key, but this report also poses the key question of to what extent Norway can domesticate its own plastic value chain, while also focussing on driving change abroad.

“There is a viable pathway for durable plastics to achieve circularity levels of over 70%, whilst reducing GHG emissions by 90%”

This data-driven study draws on analysis carried out by researchers, civil society organisations, companies, and government agencies. It has been guided by an independent and diverse Expert Panel with representation from all sectors. The model and scenario analysis from now until 2040 creates a picture of the current issues and what is needed in order to change the system trajectory, which we hope will help sector leaders and government decision makers identify effective ways to transition towards a highly circular, low-emissions plastic system.

Key Findings

The 8 key findings of the reporta are grouped into three sections (which are summarised in the infographic Exhibit 1):

Where is the system today and what trajectory is it currently on?

How to operationally change the system trajectory?

What is needed to change the system from a governance, economic, labour and user perspective?

Where is the system today and what trajectory is it currently on?

Plastics have been a key enabler of growth in our economy, which together utilised ~380,000 tonnes of plastic in 2020 across the sectors analysed. However, the system is only 21% circular and requires better management to deliver benefits to society and the economy while mitigating negative climate, environmental and social impacts.

Plastics have been a key enabler of growth in our economy, which together utilised ~380,000 tonnes of plastic in 2020 across the sectors analysed. However, the system is only 21% circular and requires better management to deliver benefits to society and the economy while mitigating negative climate, environmental and social impacts.

Plastic has been an instrumental material to our economy and society by providing, for example, key infrastructure in aquaculture, building blocks of fibres in textiles, insulation in houses, high performance form factors for electronics, and light-weighting of cars. However, these benefits to the economy and society need to be captured while mitigating plastic’s negative environmental and climate impacts.

Almost four-fifths of today’s plastic system is linear, in which ~96% of GHG emissions are generated from unabated plastic production and end-of-life incineration. This is an inefficient use of both resources and Norway’s remaining 1.5-degree carbon budget.

The Norwegian plastic system is on an unsustainable trajectory that risks exacerbating today’s systemic challenges.

The use of durable plastic (defined here as products with average lifetime of over one year) face additional challenges. It is necessary to address legacy plastics that were designed without circularity in mind, while also designing for end-of-life reuse and recycling technologies and systems operating in the future, that likely do not yet exist.

Due to continued increase in demand for plastics and the long lifetimes in these sectors, ~4.9 million tonnes of plastic stock has already accumulated in use in the system.

Environmental impacts are set to worsen in the coming years as accumulated legacy plastic starts to churn out in higher volumes than today.

If nothing changes, yearly waste volumes are forecasted to more than double by 2040, for which the existing waste infrastructure in Norway is not equipped, and over 70% of waste will be incinerated, landfilled or leaked into nature and GHG emissions will increase by an estimated 28%. This will be mainly driven by higher volumes of incineration (94%) and increased demand for virgin plastic (37%) under business-as-usual.

Current policy and industry commitments are still not ambitious enough to drive a holistic transformation of the system and to meet the European Green Deal, the Circular Economy Action Plan, and the Paris Accord.

Despite the growing attention that plastics have received in recent years, commitments made vary by sector, but Construction, Automotive, and Waste Electrical and Electronic (WEEE) are particularly falling short and are currently

not on track to meet circularity targets. Of the 16 policy and industry commitments identified, only 2 met the criteria for inclusion in the baseline “Current Commitments” Scenario. If nothing changes beyond these current

commitments, the system will be only 31% circular by 2040, a modest improvement on the 21% circularity level today, and achieve only a mere 7% reduction in GHG emissions.

How to operationally change the system trajectory?

Approximately 77% circularity can be achieved in the Norwegian durable plastic system by 2040, which would halve GHG emissions. This System Change Scenario requires a framework of ambitious circularity interventions along the plastic value chain, including the scale-up of 4 elements:

Reduction: elimination, lifetime extension, and new delivery models enabling the sharing and reutilisation of plastic can avoid up to 26% of demand.

Collection & sorting: collection for recycling as well as (local) sorting and cleaning capacity should be scaled up across all sectors as this often creates recycling bottlenecks. Extended producer responsibility (EPR) and other policies will be needed to make this economically feasible, including investments into new advanced technologies.

Mechanical recycling: a combination of design for recycling, stimulating demand for recycled content, and the scaling up of (local/regional) recycling capacity can increase mechanical recycling to ~34% and chemical recycling to 16% of total demand for utility, but is challenging because of complex polymer mixes.

Chemical recycling can offer the opportunity to boost circularity levels and deliver virgin-quality polymers, but must be complementary to the expansion of mechanical recycling and action must be taken to abate GHG emissions from the start.

Unlike for consumables, substitution with other materials, including biodegradables, were not identified at-scale for plastics in durable applications, but this could change in the future.

The application of these interventions must be tailored to each sector and, due to longer plastic lifetimes for durables, strategies to turn the system circular will have a significant time lag compared to consumables.

Construction:

The most impactful lever is maximising on-site sorting of plastic waste to ensure clean material streams and thus a higher chance of material recovery. This should be coupled with the scaling up of sorting and recycling infrastructure in Norway to treat higher volumes of sorted waste.

Reuse and reduction opportunities via innovative building design should also be leveraged to minimise demand from the sector. However, the impact of these levers on waste generation before 2040 is limited given the long in-use lifetimes.

Textiles:

As a net importer of textiles, Norway has limited control over upstream solutions and therefore close collaboration with the EU to target the production phase and support international rules and standards is key.

This can unlock a well-functioning system if combined with demand side reduction through reuse and repair business models, scaling up collection, sorting and pre-processing, and investing in new recycling technologies.

WEEE:

While recycling rates are higher compared to most other sectors, the system remains predominantly linear, largely as a result of industrial cables being left in nature, incorrect disposal of WEEE in mixed municipal solid waste, and theft from collection centres.

To achieve higher levels of circularity, leakage of waste must be reduced by maximising formal collection, with a particular focus on collecting and identifying items for reuse.

Furthermore, design for recycling principles must be adopted to reduce and standardise the types of polymers used and enable a more straightforward sorting process.

Finally, investment should be directed at scaling up innovative sorting technologies that yield higher recovery rates.

Automotive:

Although Norway is a frontrunner in terms of vehicle collection, in the current system 99% of plastics are being disposed of via landfill or incineration. Key levers to achieve circularity include adopting new business models to reduce plastic demand as well as regulation to enable a well-functioning recycling infrastructure.

Collaboration with Nordic countries (especially Sweden) will be key as Norway has no vehicle recycling facilities and volumes are too small to justify the large investments in recycling infrastructure that are required.

Fisheries & Aquaculture:

Key levers include lifetime extension in aquaculture by using gear in ways that avoid wear and tear and identifying opportunities for using gear for longer, followed by creating closed (local) recycling loops for rigid High Density Polyethylene (HDPE), and expanding the collection and depolymerization of nets.

Even after the application of these circularity levers, about half the total emissions related to plastic (~700,000 tonnes CO2eq) still remain in 2040.

To establish a trajectory in line with the net-zero pathway, additional technology interventions need to be deployed to abate the emissions from production and incineration. The Net-Zero Scenario shows that combined circularity and supply side abatement technologies can reduce emissions in 2040 by ~90% relative to Current Commitments.

Three key abatement strategies are required to achieve this (on top of the circularity levers included in the System Change Scenario):

i) switching feedstock source from fossil to alternative carbon feedstocks (such as sustainable biomass) and green hydrogen;

ii) using only renewable energy sources; and

iii) putting in place carbon capture utilization & storage (CCUS) in production and incineration facilities.

Norway is already pioneering carbon capture in its incinerators and can seek to roll this technology across is broader portfolio to abate end of life plastics emissions.

What is needed to change the system from a governance, economic, labour and user perspective?

Building a low-emissions, highly circular system requires an annual incremental investment of NOK ~280 million, which is affordable compared to scaling up a linear, resource inefficient system.

This is driven primarily by scaling up recycling infrastructure, and abating production and end-of-life emissions. A low-emissions circular system can be achieved while sustaining existing system

employment levels to 2040 (noting that the majority of jobs today are outside of Norway, and depending on the selected strategy, some could be domesticated).

However, the application of circularity

strategies will result in many jobs needing to shift from traditional volume-based production roles to circular economy-focused roles, particularly in recycling. This will require retraining to ensure a just transition.

To accelerate the transition to a low-emissions, highly circular plastic economy in Norway, a system vision and strategy needs to be defined, owned and implemented.

Today, different stakeholders in the plastic system are often working in silos and on fragmented solutions, resulting in incompatible strategies and inefficiencies.

Norway could consider setting up a multi-stakeholder transformation body to help coordinate the cross-sector cross-value chain transition strategies.

This would guarantee that the system overall balances upstream, downstream and value chain abatement interventions in a way that encourages the most resource- and cost-efficient system transition.

In order to remain a global leader in the low-emissions, circular plastic space, Norway should apply a combination of ambitious upstream and downstream circularity levers across the different sectors, enabled by a favourable policy, financial and labour environment.

The next three to five years are critical because the strategic decisions Norway makes today will determine the speed and direction of this transition for decades to come.

“The next 3-5 years are critical because the strategic decisions Norway makes today will determine the speed and direction of this transition for decades to come.”

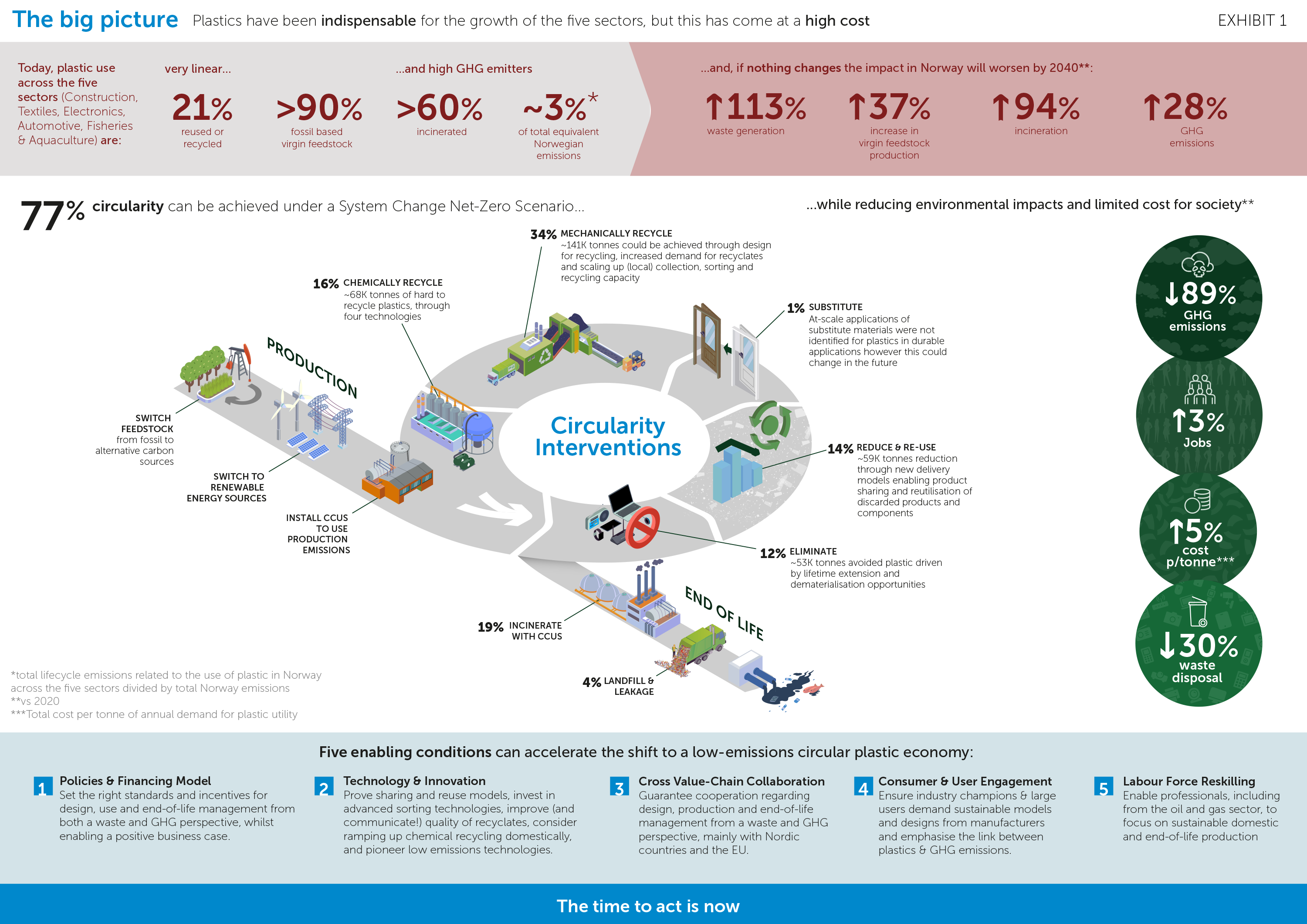

EXHIBIT 1

THE BIG PICTURE

(For Durable Plastics)

Plastics have been indispensable for the growth of the five sectors, but this has come at a high cost.

Today, the use of plastic across the five sectors (Construction, Textiles, Electronics, Automotive, Fisheries & Aquaculture) is:

very linear…

21

%

Reused or Recycled

x

90

%

Fossil based virgin feedstock

…and high GHG emitting

60

%

is incinerated

x

3

%

of total equivalent

Norwegian emissions*

…and if nothing changes the impact in Norway will worsen by 2040**:

113

%

Increased waste generation

37

%

Increased virgin feedstock production

94

%

Increased incineration

28

%

Increased GHG emissions

77% circularity can be achieved under a System Change Net-Zero Scenario…

…while reducing environmental impacts and limiting the cost for society**

*total lifecycle emissions related to the use of plastic in Norway across the five sectors divided by total Norway emissions

**vs 2020

***Total cost per tonne of annual demand for plastic utility

Five enabling conditions

can accelerate the shift to a low-emissions circular plastic economy:

1

Policies & Financing Model

Set the right standards and incentives for design, use and end-of-life management from both a waste and GHG perspective, whilst enabling a positive business case.

2

Technology & Innovation

Prove sharing and reuse models, invest in advanced sorting technologies, improve (and communicate!) quality of recyclates, consider ramping up chemical recycling domestically, and pioneer low emissions technologies.

3

Cross Value-Chain Collaboration

Guarantee cooperation regarding design, production and end-of-life management from a waste and GHG perspective, mainly with Nordic countries and the EU.

4

Consumer & User Engagement

Ensure industry champions & large users demand sustainable models and designs from manufacturers and emphasise the link between plastics & GHG emissions.

5

Labour Force Reskilling

Enable professionals, including from the oil and gas sector, to focus on sustainable domestic and end-of-life production.

The time to act is now

Download a shareable infographic