Substitute plastic wherever feasible and beneficial to prevent an additional 7% of plastic generation by 2040

In parallel to reduction, Norway should harvest the potential for the substitution of plastic wherever it can be undertaken at no cost to society or the environment. Material substitution is a complex topic that requires careful examination at the product level to understand performance, convenience and cost, as well as unintended consequences. In this report, only two material substitution strategies were considered: paper and compostable materials. These two materials were selected because they are the most prevalent for replacing single-use packaging. This system intervention refers only to substituting singleuse plastics with other single-use materials; using metal or glass as multi-use substitutes can be legitimate but is included under System Intervention #1. It is important to note that our analysis on substitution should not be considered predictions of change or recommendations, but indicative of the future scaling of existing materials assuming no unintended consequences. Therefore, a key enabling condition is for the feedstock for these two materials to be sustainably sourced (including sound land and water management) and recycling rates to remain high.

In a globalised system of food production and consumption, the GHG emission savings offered by lightweight plastic materials are important. However, if supply chains are shortened, transport is decarbonised, or reuse and recycling rates are high, other substitute materials – such as glass and metals – can perform well. Life cycle analysis on a product-by-product basis should remain the standard for science-based decision-making processes when it comes to substitution.

For our analysis, compostables are defined as materials capable of disintegrating into natural elements in a home or industrial composting environment within a specified number of weeks, leaving no toxicity in the soil according to credible international standards. Compostables are most relevant where food waste processing infrastructure exists or will be built, and for substituting thin plastic films and small formats. Substitution with compostable materials is most appropriate for products with low plastic recycling rates and high rates of food contamination, making coprocessing with organic waste a viable option. Given the specificity of the Norwegian context – such as high food-waste sorting at source, cold weather leading to low potential for home composting, and a heavy reliance on anaerobic digestion for food-waste processing – the potential of compostable materials has been adjusted to exclude target materials and applications that typically take longer to degrade (e.g. thicker products and poly(lactic acid)).

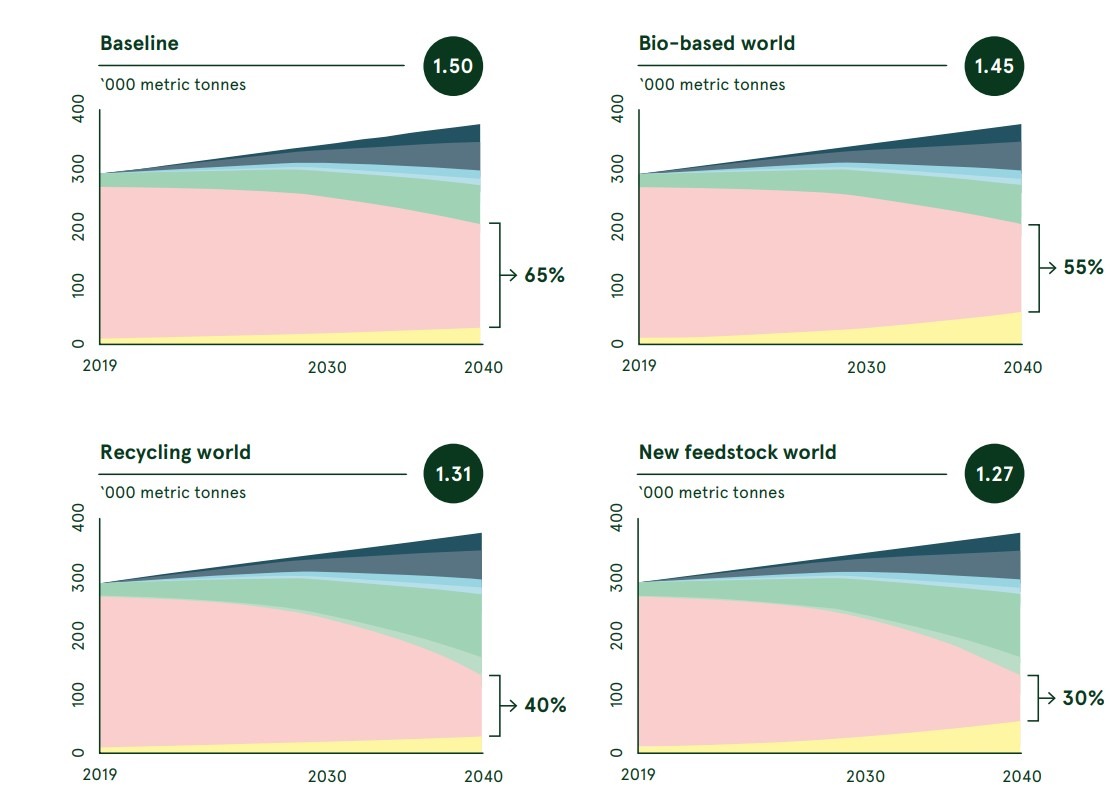

Our analysis found that up to 15,000 tonnes (mostly of packaging), can be substituted with paper and up to 10,000 tonnes with compostables. Non-food contact applications, and dry food applications where water barrier properties are not necessary, including postconsumer films, have one of the highest substitution potentials (10,000 tonnes), followed by rigid packaging (10,000 tonnes) mostly comprised of pots, tubs and trays, and B2B films and carrier bags (2,000 tonnes). For more information on this analysis, please see the technical report.

Examples of applications with the highest potential for reduction are:

- Use of concentrated capsules for household cleaners, soaps, or even toothpaste

- Moving from liquid to solid cosmetics

- Packing reusable water bottles and bags

- Drinking off-premises coffee or tea from a reusable cup

- Scaling up the use of soda and/or sparkling water dispensers

- Trialing edible packaging alternatives for food and drinks

- Ordering online shopping, groceries, or meals in reusable boxes and containers

- Shopping from in-store displaying bulk dispensers and plastic-free aisles

- Shifting from disposable to reusable diapers

- Encouraging business-to-business development of closed loop and/or re-use systems for secondary and tertiary packaging (e.g. crates).

While this system intervention requires that consumers shift their behaviour, the role of consumer goods companies and governments is even more important.

- Consumer goods companies and retailers have the most prominent role in ensuring that:

– They adopt regulatory or standard requirements for plastic packaging that focus on the elimination of avoidable packaging.

– They scale-up supply chain innovation, such as the use of seasonal food, local suppliers, digital trackers, and choice editing (reducing the need for packaging to differentiate products).

– Consumers are offered the choice to consume differently. R&D programmes and pilots must be implemented to identify which existing solutions could be culturally accepted in Norway and the impact of each one on a product-by-product basis.

- The central government can also play a role by shifting the burden of the cost of waste management towards producers through different policies, such as legally binding extended producer responsibility (EPR), and legally binding taxes on single-use plastic and wasteto-energy incineration. New policies will need to meet the requirements set out in the relevant EU legislation.

Overall, it is worth noting that the substitute materials in this category come at a higher cost (up to 2 times more when including production and packaging conversion). Ensuring the development of substitute materials at scale in Norway relies on several enabling conditions:

- The central government supporting the development of research and innovation in the field of alternative materials for single-use plastic packaging and problematic materials or formats (see System Intervention #10).

- The central government, as well as other EU governments:

– Supporting the development of standards which clearly define acceptable composting materials according to locally available management system and providing clarity around the word “biodegradable”.

– Promoting certification schemes for the sustainable sourcing of biomass and the adoption of strict criteria by brands and producers to ensure that substitutes contain recycled content and are sourced responsibly.

– Implementing policies and voluntary commitments to accelerate the expansion of paper collection and recycling, increase recycled content in paper, reduce contamination, and scale separate organic waste treatment that can accept compostable packaging.

- The financial sector recognising the space as financially viable with economic opportunities. In accordance with the Circular Economy Action Plan, the European Commission is currently assessing applications where using biodegradable and compostable plastics can be beneficial to the environment, and the criteria for their use. Further policy development in this area is expected.