Fossil

Free

Plastics

Fossil-free plastics present a strategic opportunity for Europe’s industrial resilience

Europe’s plastic system is at a turning point.

Plastics underpin essential sectors, from healthcare and food to construction and transportation. But in Europe, nearly 80% of plastics are produced from virgin fossil feedstocks. Without action, plastic production and disposal in Europe could emit up to 180 Mt CO₂eq/year by 2050 – a 30% rise from today.

Even with the most ambitious ‘reduce-reuse-recycle’ measures, up to 28 million tonnes of virgin fossil plastic will still be needed in Europe each year to meet market demand. Without alternative, fossil-free feedstocks, that demand will lock in further fossil emissions.

Fossil-free virgin plastics are an essential part of the solution.

RESOURCES

DEVELOPED BY

COMMISSIONED BY VIONEO

The case for fossil-free plastics.

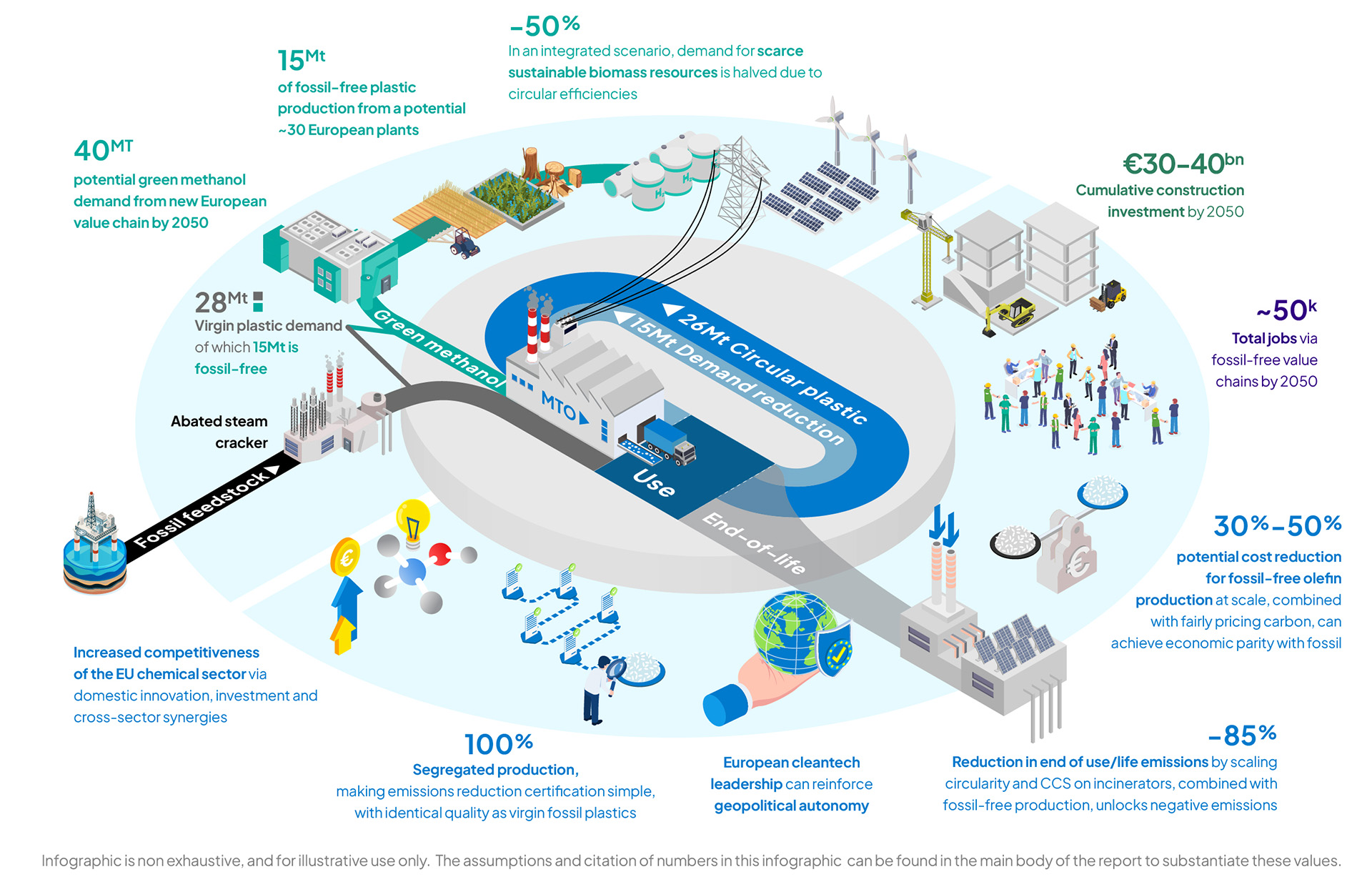

Systemiq’s new report, Fossil-Free Plastics: Driving Clean Industrial Leadership in Europe, makes the case for accelerating fossil-free production using scalable, drop-in technologies such as green methanol-to-olefins (MTO). This pathway produces high-quality, recyclable plastics (polyethylene and polypropylene) from renewable carbon sources – offering identical performance to fossil-based products, but with traceability and lower emissions.

GHG reduction impacts at value chain and system level

5−7 tCO₂eq emissions reduction vs existing pathways

Fossil-free plastics integrated with circularity & carbon management can achieve a net zero plastics system most efficiently and reliably

Fossil-free plastics could drive net negative emissions if CCS is applied to incinerators

To fully reflect the negative emissions potential of fossil-free plastics, PCF methods should adopt the -1/+1 cradle-to-grave approach

Socio-economic impacts

Fossil-free plastics at scale can achieve cost parity with abated fossil production

Scaling up fossil-free plastics can attract substantial investment in European manufacturing, generate jobs, and accelerate the development of net-zero value chains

Growing demand for green methanol, driven by fossil-free plastics, can help move European projects closer to final investment decisions

Strategic and industrial resilience impacts

For customers, fossil-free plastics produced via MTO deliver identical quality as virgin fossil plastics, with fully segregated traceability throughout the supply chain

By enabling cross-sector synergies and boosting geopolitical autonomy, the development of fossil-free plastics can reinforce Europe’s cleantech leadership

Fossil-free plastics can drive domestic innovation and boost the competitiveness of the EU chemical sector, while also de-risking the industrial transition to net-zero

Priority sectors for early action

The report identifies automotive and medical applications, and food-grade packaging as near-term priority sectors where quality and regulatory requirements limit the use of recycled content. These high-spec applications represent ideal beachheads for fossil-free plastics – offering immediate climate impact and brand value for early adopters.

Companies are preparing to scale this pathway – but uncertainty around market demand and policy signals is holding back investments and first production projects from becoming a reality.

Four stages to unlock scale.

The report highlights four stages to enable successful market formation and scale-up of fossil-free plastics.

A cornerstone of Europe’s clean industrial future

With the right policy and business leadership, fossil-free plastics can play a central role in a net-zero aligned, circular, and globally competitive plastics system – helping Europe lead the shift to green materials while reducing its reliance on fossil fuels.

Fossil-free plastics in a circular, net-zero emissions European plastics system

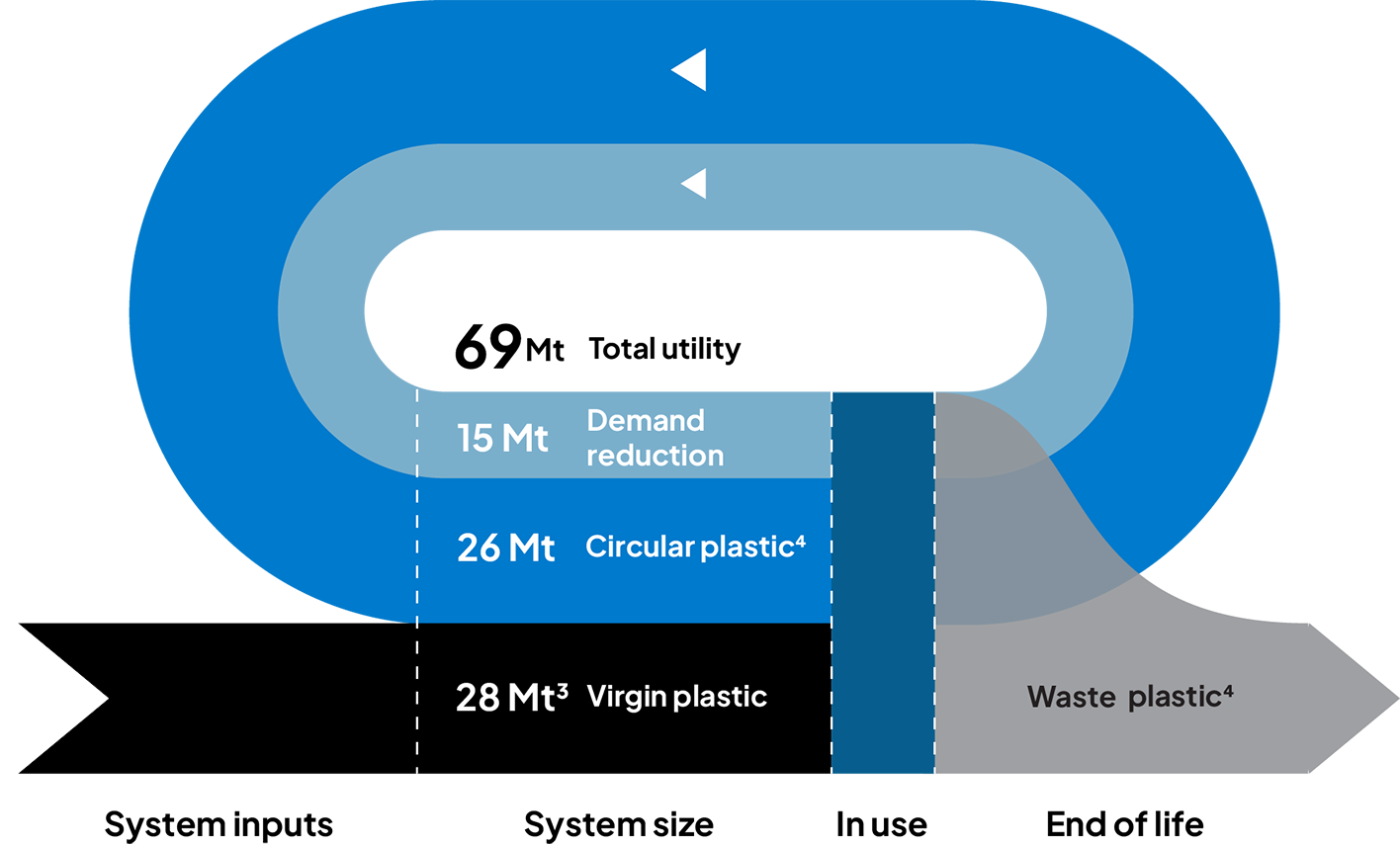

European plastics system | the state of play today

54

Mt

of plastic demand in the European system today

80

%

of plastic produced from virgin fossil feedstocks and only 1% from bio-based feedstocks, with the remainder from recycling

5

tCO₂eq

GHG emissions per tonne of plastic produced, (if incinerated)

140

MtCO₂eq

GHG emissions per year, rising by 30% by 2050 in a Business-as-usual scenario

A 2050 Integrated Scenario combines fossil-free plastic production with circularity and carbon management along the value chain

In an Integrated Scenario in 2050, the European plastics system can achieve net zero with the greatest resource efficiency and lowest transition risk

69

Mt

of plastic utility is required by 2050. Circularity measures of elimination, reuse, and substitution reduce demand by 15Mt, leaving 54Mt of plastic needed to deliver the same utility

50

%

of virgin plastics produced from fossil-free feedstocks, equating to ~55%

-

2

tCO₂eq sequestration per tonne of fossil-free plastic cradle to grave, driving 5−7 tonnes of emissions reduction vs fossil plastic today

Net zero

emissions, with residual positive system emissions compensated for by fossil-free negative emissions

To make fossil-free plastics a reality in Europe, four stages to unlock scale are required:

Build first projects by mobilising pioneer customers

Announce bold industrial strategy to establish the relevance of fossil-free plastics in Europe’s future

Establish clear market foundations to define and

clearly account for the value of fossil-free plastic

Provide structural market support to stimulate demand, level the playing field with fossil and provide public support for early market development

ACKNOWLEDGEMENTS

The report was commissioned by Vioneo and developed independently by Systemiq. It builds on Systemiq’s established modelling of plastics and chemicals transitions and incorporates input from an expert panel including voices from academia, civil society, and industry.

WEBINAR

REPORT WALKTHROUGH

ENDORSEMENTS

Further reading…